accumulated earnings tax c corporation

A corporation can accumulate its earnings for a possible expansion or other bona fide business reasons. The IRS introduced new forms Schedules K-2 and K-3 for pass-through entities and filers of Form 8865 Return of US.

How Corporations May Run Afoul Of The Accumulated Earnings Tax A Section 1202 Planning Brief Frost Brown Todd Full Service Law Firm

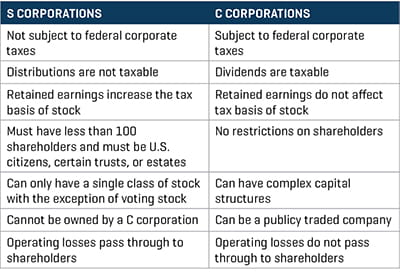

However the taxation of distributions is more complicated if the S corporation has C corporation accumulated earnings and profits EP.

. If the amount of the dividend paid out exceeds the sum of both current EP and accumulated EP then. For purposes of paragraph 2 a distribution made by a foreign corporation out of its profits which are attributable to a distribution received from a foreign corporation to which former section 902b of the Internal Revenue Code of 1986 formerly IRC. An S corporation does not generate EP.

440003210094 CT-3-S 2021 Page 3 of 6 Composition of prepayments see instructions. Accumulated EP is a tax term for what under financial accounting is called retained earnings. EP generated in a C corporation are.

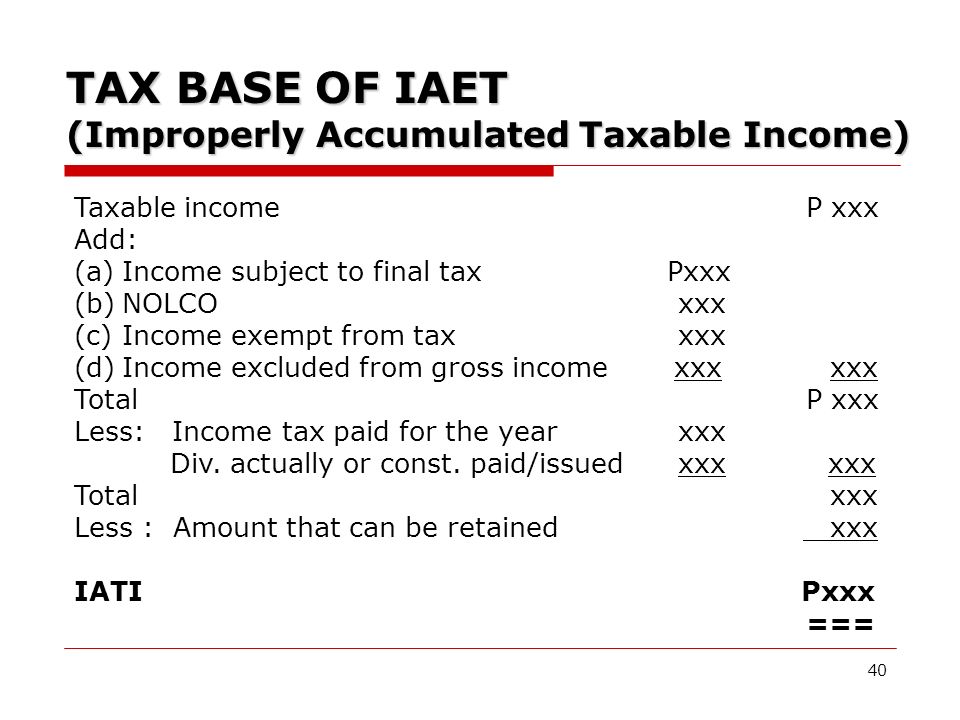

The effective income tax rate for the second quarter of 2022 was 222 compared to 200 in the same period of 2021. Generally the E. The accumulated earnings tax may be imposed on a corporation for a tax year if it is determined that the corporation has attempted to avoid tax to its shareholders by allowing its EP to.

S corporations in general do not make dividend distributions. Accumulated earnings and profits are a companys net profits after paying dividends to. Material Changes 1 The following IRM sections have been added to incorporate the provisions of Interim Guidance Memorandum SBSE-04-0915-0056 Interim Guidance on Access to Suspicious Activity.

C corp shareholders receive Form 1099-DIV and they will in turn report the dividend on their individual federal tax return. The accumulated earnings tax is a 20 penalty that is imposed when a corporation retains earnings beyond the reasonable needs of its business ie instead of paying dividends with the purpose of avoiding shareholder-level tax seeSec. A regular C corporation distributing its earnings out of retained earnings is considered a dividend.

A In general In the taxable year when paid if the contributions are paid into a pension trust other than a trust to which paragraph 3 applies and if such taxable year ends within or with a taxable year of the trust for which the trust is exempt under section 501a in the case of a defined benefit plan other than a multiemployer plan in an amount determined under subsection o. Distribution from S Corporation Earnings. The department uses the.

Federal tax purposes and. In periods where corporate tax rates were significantly lower than individual tax rates an. C corporations are subject to double taxation because profits are taxed at the corporate level when they are earned and at the individual level when they are distributed as dividends.

New York S Corporation Franchise Tax Return Tax Law Articles 9-A and 22 Employer identification number EIN File number Business telephone number. Persons With Respect to Certain Foreign Partnerships to standardize international tax reporting of international business activities or foreign partners for tax years 2021 and thereafter. 1954 applies shall be treated as made out of the accumulated profits of a foreign.

The difference is largely due to global intangible low-taxed income and the geographic mix of earnings. As of 2013 the top 1 of households the upper class owned 367 of all privately held wealth and the next 19 the managerial professional and small business stratum had 522 which means that just 20 of the people owned a remarkable 89 leaving only 11 of the. 901m generally applies to a target foreign corporation for which a Sec.

4104 Examination of Income Manual Transmittal. In the United States wealth is highly concentrated in relatively few hands. Except as otherwise provided in this paragraph the term accumulated adjustments account means an account of the S corporation which is adjusted for the S period in a manner similar to the adjustments under section 1367 except that no adjustment shall be made for income and related expenses which is exempt from tax under this title and.

If the accumulated earnings tax applies interest applies. Schedule K-2 reports partners distributive shares or S. 901m disqualifies as a foreign tax credit all or a portion of the target foreign corporations eligible foreign taxes based on a ratio using the foreign corporations original basis in assets for US.

On an adjusted basis the effective income tax rates were 263 and 175 for the second quarter of 2022 and 2021 respectively. C Accumulated earnings and profits. However only the distributions made from current or accumulated EP will reduce EP.

If the corporation had tax withheld under Chapter 3 or 4 of the Internal Revenue Code and received a Form 1042-S Form 8805 or Form 8288-A showing the amount of income tax withheld attach such forms to the corporations income tax return to claim a withholding credit. Purpose 1 This transmits revised IRM 4104 Examination of Returns Examination of Income. IRC 532 a states that the accumulated earnings tax imposed by IRC 531 shall apply to every corporation other than those described in subsection IRC 532b formed or availed of for the purpose of avoiding the income tax with respect to its shareholders or the shareholders of any other corporation by permitting earnings and profits to.

23 In addition to reviewing the Schedule M-2 Analysis of Unappropriated Retained Earnings per Books from a corporations annual Form 1120 a detailed analysis of. Accumulated earnings and profits E P is an accounting term applicable to stockholders of corporations. Updated October 152020.

However if a corporation allows earnings to accumulate beyond the reasonable needs of the business it may be subject to an accumulated earnings tax of 20. 338g election was made. A corporation can pay a dividend either out of current EP or accumulated EP.

By law 42 USC. The Times obtained Donald Trumps tax information extending over more than two decades revealing struggling properties vast write-offs an audit battle and hundreds of millions in debt coming due. As previously discussed an S corporation can only possess accumulated EP if it was previously a C corporation or if it acquired the assets of a C corporation in a Section 381 transaction.

Code 11716 the department has the authority to use the Social Security number SSN to administer the Pennsylvania personal income tax and other Commonwealth of Pennsylvania tax laws. Tax on retained earnings C corp is a common question for those in the process of incorporating a business. Though similar they may differ because of the statutory adjustments.

Top individual tax rates are higher than top corporate rates and C corporations can retain earnings rather than passing through the entire amount so a regular corporation might wind up being the most tax-advantageous choice in some scenarios. If a corporation has too many tax preference items it may be subject to AMT or Alternative Minimum. However it can possess EP as a result of either converting from C corporation to S corporation or acquiring a C corporation.

3 Post-1986 earnings and profits The term post-1986 earnings and profits means the earnings and profits of the foreign corporation computed in accordance with sections 964a and 986 and by only taking into account periods when the foreign corporation was a specified foreign corporation accumulated in taxable years beginning after.

2

Darkside Of C Corporation Manay Cpa Tax And Accounting

2

Determining The Taxability Of S Corporation Distributions Part Ii

2

Oh How The Tables May Turn C To S Conversion Considerations Stout

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession Ppt Download

Significant Cuts To The Corporate Tax Rate Is It More Beneficial To Be A C Corporation Now Bernard Robinson Company

What Are Retained Earnings Quickbooks Australia

What Are Accumulated Earnings Definition Meaning Example

Understanding The Accumulated Earnings Tax Before Switching To A C Corporation In 2019

Determining The Taxability Of S Corporation Distributions Part Ii

Earnings And Profits Computation Case Study

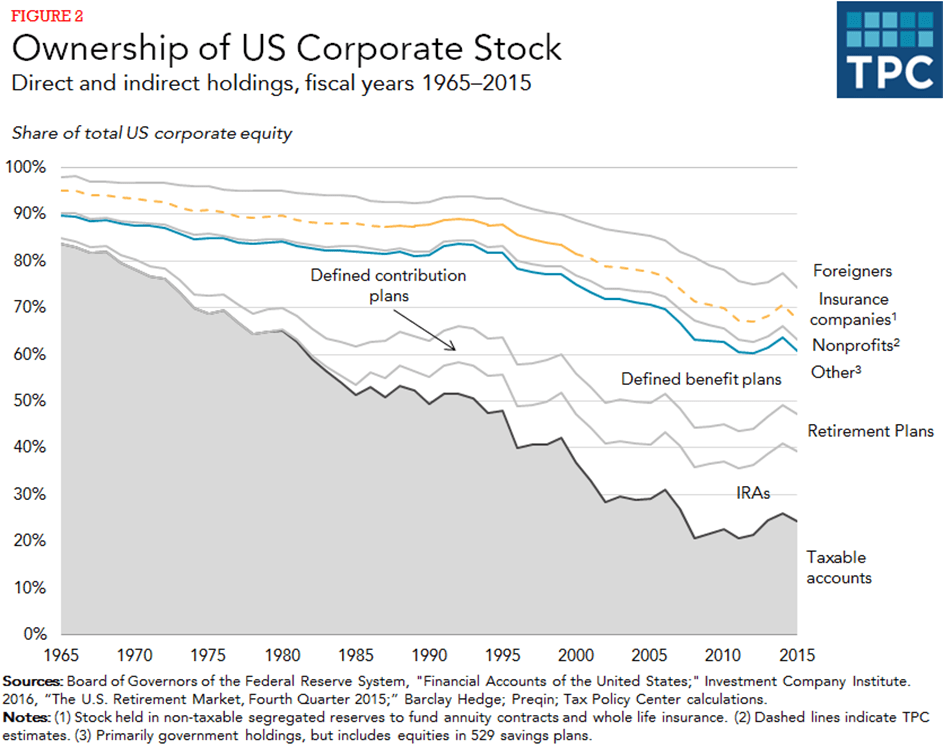

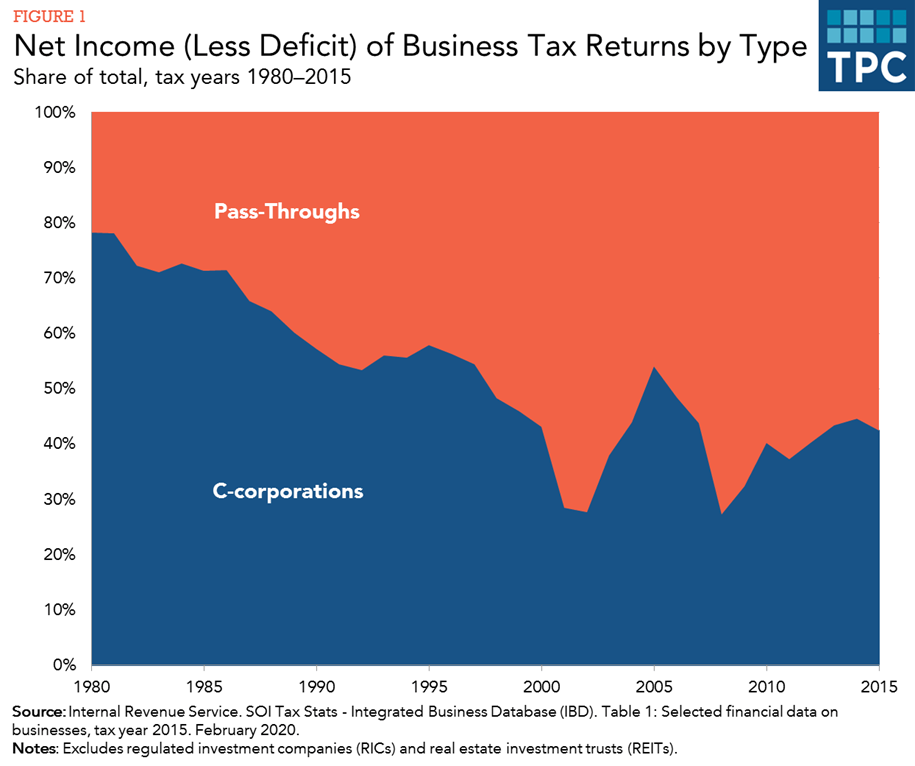

Is Corporate Income Double Taxed Tax Policy Center

Corporate Distributions

Is Corporate Income Double Taxed Tax Policy Center

Demystifying Irc Section 965 Math The Cpa Journal

Earnings And Profits Computation Case Study

Earnings And Profits Computation Case Study